Stop Livin’ On a Prayer

In our last post, we discussed the importance of developing a financial Forecast for your small business. You start by defining your long-term vision of where the business is headed. Then you break it down to the next two years (you can go longer, but generally a forecast begins to fall apart in terms of accuracy after two years). Armed with sufficient data, your trusted advisor can help you build a detailed forecast that describes your vision in numbers in a similar way that a novel tells a story with words.

Accounting is a language, and your financial forecast tells the story of where you are going, and how you are going to get there. Don’t confuse a “budget” with a “forecast.” A budget is only meaningful if it is tied to a solid forecast. A budget is simply how much financial resource you are willing to spend in a certain area of your business, within a defined time. The forecast is your entire business model, expressed in numbers and derived entirely from:

1) relevant data that you have collected about your revenue sources, costs of materials and labor, and administrative needs, and

2) your understanding of market conditions.

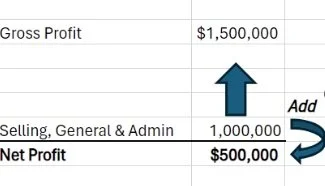

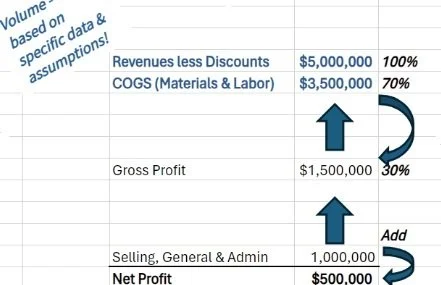

Start your financial forecast at the bottom of your income statement. That’s right, we said start at the bottom, with the line called “Net Profit.” We are going to work our way up the income statement from the bottom to the top – what we call “bottom-up forecasting.” We have found that the bottom-up approach is the most likely to yield a realistic, data-driven forecast that guarantees you will know exactly how you are going to achieve your targeted profit. So, ask yourself – how much net profit do I intend to make in this business? Be reasonable, but at the beginning don’t worry about being too high or too low – your Net Profit number will be refined by what comes next, which is...

Selling, General, and Administrative (SG&A) expenses, commonly known as “overhead.” We are assuming that most of our readers have a basic understanding of what these costs are. Generally, we tell clients to think of Overhead in three broad categories: 1) Selling and Marketing Expenses, which are highly discretionary; 2) Occupancy Costs, which tend to be fixed; and 3) Office/Administrative Expenses, which also tend to be fixed. Collectively, overhead costs are those that you cannot avoid, but are not directly tied to the delivery of your product or service to your customers.

Next, add your targeted Net Profit to your total SG&A overhead expenses. The sum is your targeted Gross Profit.

Gross Profit is easy to understand, and it can be broken down into units. It requires answers to two basic questions: how much do you charge for each unit of product or service that you sell (Revenue), and what does it cost to produce that unit (Cost of Goods Sold or “COGS”)?

Once you have your per-unit Revenue and COGS, you need to multiply both by volume – in other words, how many are you going to sell in a given period (a month, a year, etc.). This is not an easy task. Instead of doing the hard work of analyzing your expected Revenue based on a work pipeline, pre-orders, and/or knowing your customers’ demand, many business owners take the “quick and easy” approach of simply taking last year’s numbers and adding some arbitrary growth percentage. You need to get more granular than that – more detailed. Remember, this forecast is the document you use to measure success and inform your decisions.

To cover your overhead costs and make your targeted Net Profit, you need to sell a certain number of units at a certain price, and those units have a built-in cost to produce. Who are your customers going to be? How much is each going to buy, and when, and how do you know those assumptions are likely to be correct? What are you asking your sales team to do, to ensure that this level of volume is achieved? Are there any discounts involved for larger sales? Do you have volatility in your target customer market, and/or seasonality to consider?

Your trusted advisor can help you retrieve the necessary data, refine or “normalize” that data, and organize it into a forecast format (we always recommend a month-by-month P&L forecast for the next 24 months). Get a handle on it now before another year in business passes you by.